Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Home Sweet Home: The Emotional Benefits of Homeownership

![Home Sweet Home: The Emotional Benefits of Homeownership [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/11/21164928/Home-Sweet-Home-The-Emotional-Benefits-Of-Home-Ownership-MEM-1046x2152.png)

Some Highlights

- While there are many financial perks to owning a home, there are also powerful non-financial benefits to consider if you’re thinking about making a move.

- Homeownership allows you to express yourself, gives you greater privacy and comfort, enhances your connection to your community and loved ones, and is an achievement to feel proud of.

- Let’s connect today to discuss all that homeownership has to offer.

Build your net worth through equity

If you’ve set out to buy a home, you’re likely balancing your own needs with higher mortgage rates and today’s home prices. That can feel challenging. But know that making a purchase today can pay off in the long run as you build your net worth through equity.

What Buyers Need To Know About the Inventory of Homes Available for Sale

If you’re thinking about buying a home, you’re likely trying to juggle your needs, current mortgage rates, home prices, your schedule, and more to try to decide if you want to jump into the market.

If this sounds like you, here’s one key factor that could help you with your decision: there are more homes for sale today than there were at this time last year. According to Calculated Risk, for the week ending in November 18th, there were 47.7% more homes available for sale than there were at the same time in 2021. And having more options for your home search may be exactly what you need to feel confident about making a move.

Here’s a look at where the increased housing supply is coming from so you can get a better sense of what’s happening in the market today and what it means for you.

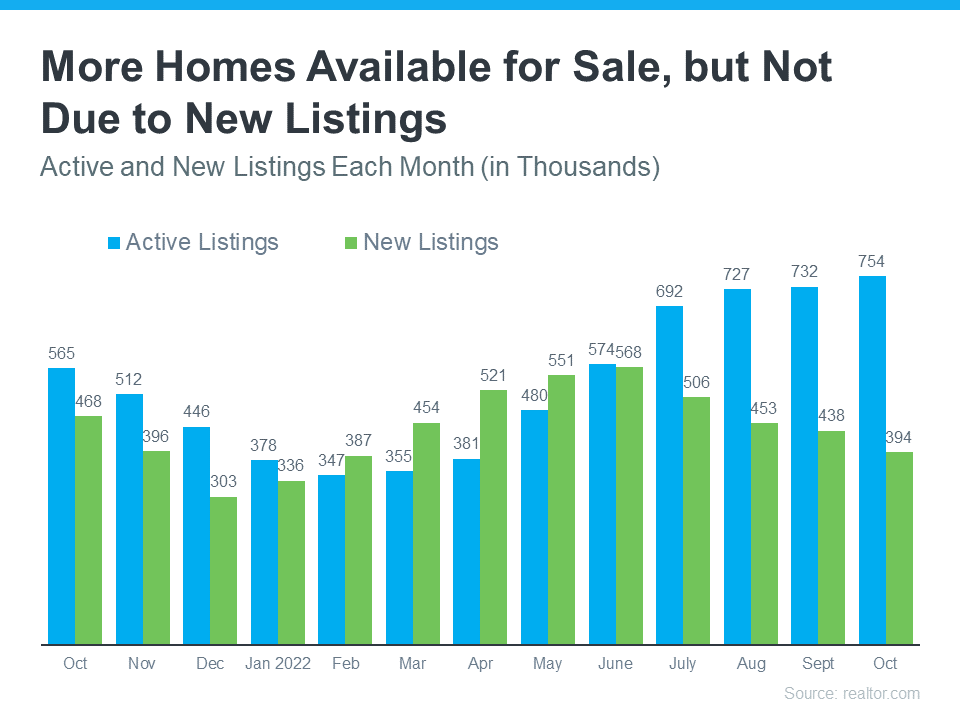

What Caused the Growth in Housing Inventory This Year?

The increase we’ve seen in housing supply this year isn’t from the source you think it is. Rather than an influx of recent homeowners listing their houses for sale (known as new listings), the primary reason the supply has grown is because homes are staying on the market a bit longer (known as active listings).

That’s happening because higher mortgage rates and home prices have helped moderate the peak frenzy of buyer demand, which has slowed down the pace of sales. And, as the pace of sales has eased, inventory has grown as a result.

The graph below uses data from realtor.com to show that it’s active listings, not new listings, that have driven the growth we’ve seen over the past few months:

And while overall inventory gains may slow down this winter due to typical housing market seasonality, you still have a chance to capitalize on the current supply.

What This Means for Your Home Search

Regardless of the source, the increase in available housing supply is good for buyers. More homes available for sale means you have more options to choose from as you search for your next home, and you may even have more time to consider them.

So, if you tried to buy a home last year and lost out in a bidding war or just couldn’t find something you liked, this may be the news you’ve been waiting for. If you start your search today, those additional options should make it less difficult to find a home you love, especially as some other buyers pause their search this holiday season.

Just remember, housing supply is still low overall, so it won’t suddenly be easy – it’ll just be less challenging than it was at this time last year. As a recent article from realtor.com says:

“Despite this improvement in the number of homes actively for sale, active listings still lag their pre-pandemic levels.”

The increase in housing supply helps put you in a great position to kick off the new year in your dream home. And who better to help you find it than a trusted, local real estate professional?

Bottom Line

If you’re ready to jump into the housing market and see what’s available in our local area, let’s connect.

More People Are Finding the Benefits of Multigenerational Households Today

If you’re thinking of buying a home and living with siblings, parents, or grandparents, then multigenerational living may be for you. The Pew Research Center defines a multigenerational household as a home with two or more adult generations. And the number of individuals choosing multigenerational living has increased over the past 50 years.

As you consider this option for your own home search, know it could help you on your homeownership journey and provide you with other incredible benefits along the way.

Living with Loved Ones Could Help You Achieve Your Homeownership Goals

There are several reasons people choose to live in a multigenerational household, and for many, the arrangement is a personal one. But according to the Pew Research Center, the top reason people choose to live together today is financial.

A recent study from Freddie Mac also finds more people are choosing to buy a home together so they can save money in the homebuying process. As the study says:

“. . . an increasing percentage of young adult first-time homebuyers are relying on support from older generations, including their parents, to buy a home together.”

For these individuals, combining their resources can help them achieve their dream of buying and owning a home. By pooling their incomes together to make that purchase, they may be able to afford a home they couldn’t on their own.

Other Key Benefits of Multigenerational Living

Not to mention, living in a home with loved ones can have other benefits too, like giving you more quality time to spend together. Darla Mercado, Certified Financial Planner and Markets Editor for CNBC.com, explains how this living arrangement can help on a personal and financial level:

“Residing with relatives can offer advantages . . . you can pool multiple streams of income, for instance. And in households with young children, grandparents can pitch in with child care.”

If this sounds like a great option for you, it’s important to work with a trusted real estate professional to discuss your needs. They can help you navigate the process to find the right home for you and your loved ones.

Bottom Line

More people are discovering the benefits of multigenerational living. For the best information and help deciding what’s right for your personal situation, let’s connect and start the conversation today.

Should You Update Your House Before You Sell? Ask a Real Estate Professional.

![Should You Update Your House Before You Sell? Ask a Real Estate Professional. [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/11/16134552/Should-You-Update-Your-House-Before-You-Sell-Ask-A-Real-Estate-Professional-MEM-1046x2648.png)

Some Highlights

- You may be wondering what needs to be renovated before you sell your house. In today’s shifting market, making your house appealing is more important than ever.

- That’s why it’s essential to lean on a real estate professional who has in-depth knowledge of today’s housing market. They know what buyers are looking for and how to highlight any upgrades you make.

- Let’s connect so you know where to focus your efforts so your house will stand out in a today’s market.

Mortgage Rates Will Come Down, It’s Just a Matter of Time

This past year, rising mortgage rates have slowed the red-hot housing market. Over the past nine months, we’ve seen fewer homes sold than the previous month as home price growth has slowed. All of this is due to the fact that the average 30-year fixed mortgage rate has doubled this year, severely limiting homebuying power for consumers. And, this month, the average rate for financing a home briefly rose over 7% before coming back down into the high 6% range. But we’re starting to see a hint of what mortgage interest rates could look like next year.

Inflation Is the Enemy of Long-Term Interest Rates

As long as inflation is high, we’ll see higher mortgage rates. Over the past couple of weeks, we’ve seen indications that inflation may be cooling, giving us a glimpse into what may happen in the future. The mortgage market is eagerly awaiting positive news on inflation. As Ali Wolf, Chief Economist at Zonda, says:

“The housing market is expected to face continued uncertainty heading into 2023 as consumers, financial markets, and policymakers work through their respective challenges in today’s economy. . . . we are watching for any additional stability in the MBS market, signs of cooling inflation, and/or less aggressive Federal Reserve action to give us confidence that mortgage rates are past their peak.”

What Does This Mean for the Future of Mortgage Rates?

As we get through the inflation battle and start to see that coming down, we should expect mortgage rates to follow. We’ve seen nods of this over the past couple of weeks. As the Federal Reserve works to bring inflation down, mortgage rates will come down as well. Bill McBride from Calculated Risk says:

“My current view is inflation will ease quicker than the Fed currently expects.”

As we look toward next year, we certainly hope he’s right.

Bottom Line

Mortgage rates will come down – it’s just a matter of time. The hope is we continue to see more positive news on inflation, and that’ll bring mortgage rates down. This will give prospective homebuyers more buying power and lead to more homeowners throughout the country.

What Homeowners Want To Know About Selling in Today’s Market

If you’re thinking about selling your house, you’re likely hearing about the cooling housing market and wondering what that means for you. While it’s not the peak intensity we saw during the pandemic, we’re still in a sellers’ market. That means you haven’t missed your window. Realtor.com explains:

“. . . while prospective home sellers may lament that they missed their prime window, in reality, this is still a terrific time to sell. In fact, according to a recent Realtor.com® home seller survey, 95% of sellers who sold their home in the past year got more than they paid for it.

Nonetheless, some of the more prominent pandemic trends have changed, so sellers might wish to adjust accordingly to get the best deal possible.”

The key to success today is being realistic and working with a trusted real estate advisor who can help you set your expectations based on where the market is now, not where it was over the past few years.

Here are a few things experts say today’s sellers need to consider.

Be Willing To Negotiate

At the peak of the pandemic frenzy, sellers held all the leverage because inventory was at record lows and buyers were willing to enter bidding wars over homes that were available. This year, the supply of homes for sale has increased as the market cooled. Even though inventory is still low overall, buyers today have more options, and with that comes more negotiation power.

As a seller, that means you may see more buyers getting an inspection, requesting repairs, or asking for help with closing costs today. You need to be prepared to have those conversations. As Ali Wolf, Chief Economist at Zonda, says:

“Today’s market is different than it was just six months ago. . . Sellers that want the contract to move forward should be willing to work with the buyer. . . Consider helping with the closing costs or addressing many of the items on the home inspection list.”

Price Your Home at Market Value

It’s not just that the number of homes for sale has grown this year. Buyer demand has also pulled back in light of higher mortgage rates. As a result, pricing your house appropriately so you can catch the eyes of serious buyers is important. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Price your home realistically. This isn’t the housing market of April or May, so buyer traffic will be substantially slower, but appropriately priced homes are still selling quickly.”

You don’t want to overreach with your price and deter buyers. At the same time, you don’t want to undervalue your home and leave money on the table. This is another area where an agent’s expertise comes in handy.

Think About Your First Impression on Buyers

Buyers have more options and are more particular about their investment since it costs more to buy a home given today’s mortgage rates. As a result, you need to make sure your house shows well. As an article from realtor.com says:

“To stand out in the market, sellers should make their home attractive to buyers, which usually means some selective updates.”

This could include everything from staging the home, to making small cosmetic updates, tackling repairs, or undergoing renovations. A trusted real estate professional will help you assess what may be worthwhile to do compared to other recently sold homes in your area.

Bottom Line

To sum it all up, your house should still sell today and move quickly if you’re realistic about today’s market. As a press release from Zillow puts it:

“. . . sellers need to do things right to attract the attention of these buyers — pricing their home competitively and making their listing attractive to online home shoppers.”

For expert advice on how to quickly sell your house in a shifting market, let’s connect.

Top Questions About Selling Your Home This Winter

There’s no denying the housing market is undergoing a shift this season, and that may leave you with some questions about whether it still makes sense to sell your house. Here are three of the top questions you may be asking – and the data that helps answer them – so you can make a confident decision.

1. Should I Wait To Sell?

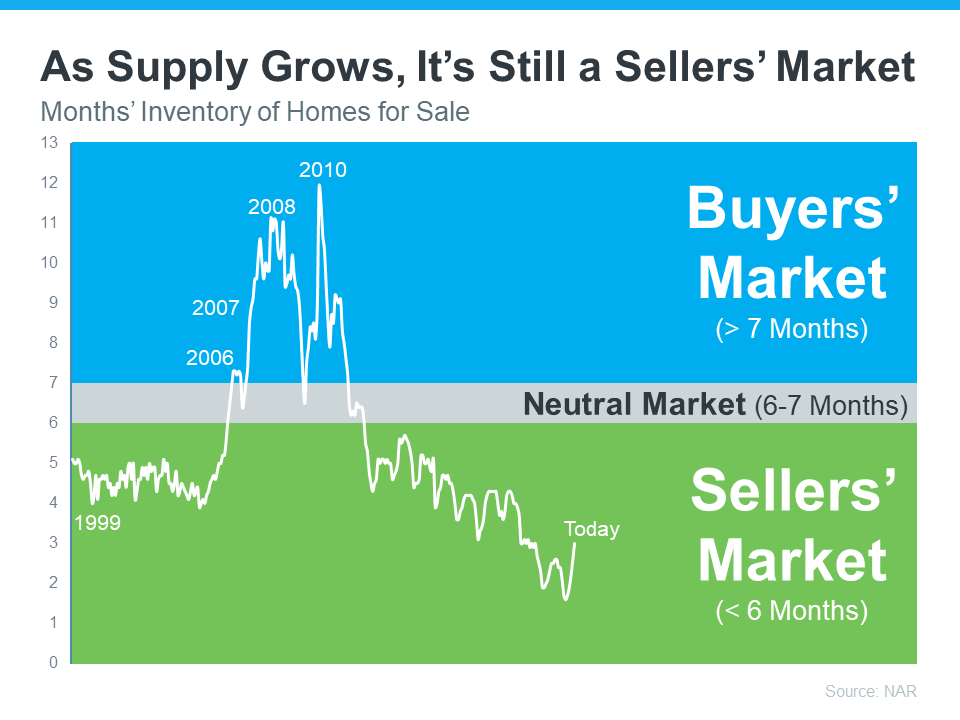

Even though the supply of homes for sale has increased in 2022, inventory is still low overall. That means it’s still a sellers’ market. The graph below helps put the inventory growth into perspective. Using data from the National Association of Realtors (NAR), it shows just how far off we are from flipping to a buyers’ market:

While buyers have regained some negotiation power as inventory has grown, you haven’t missed your window to sell. Your house could still stand out since inventory is low, especially if you list now while other sellers hold off until after the holiday rush and the start of the new year.

2. Are Buyers Still Out There?

If you’re thinking of selling your house but are hesitant because you’re worried buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As an article in Forbes explains:

“At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.”

While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. If you’re wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for.

3. Can I Afford To Buy My Next Home?

If current market conditions have you worried about how you’ll afford your next move, consider this: you may have more equity in your current home than you realize.

Homeowners have gained significant equity over the past few years and that equity can make a big difference in the affordability equation, especially with mortgage rates higher now than they were last year. According to Mark Fleming, Chief Economist at First American:

“. . . homeowners, in aggregate, have historically high levels of home equity. For some of those equity-rich homeowners, that means moving and taking on a higher mortgage rate isn’t a huge deal—especially if they are moving to a more affordable city.”

Bottom Line

If you’re thinking about selling your house this season, let’s connect so you have the expert insights you need to make the best possible move today.

Home Equity: A Source of Strength for Homeowners Today

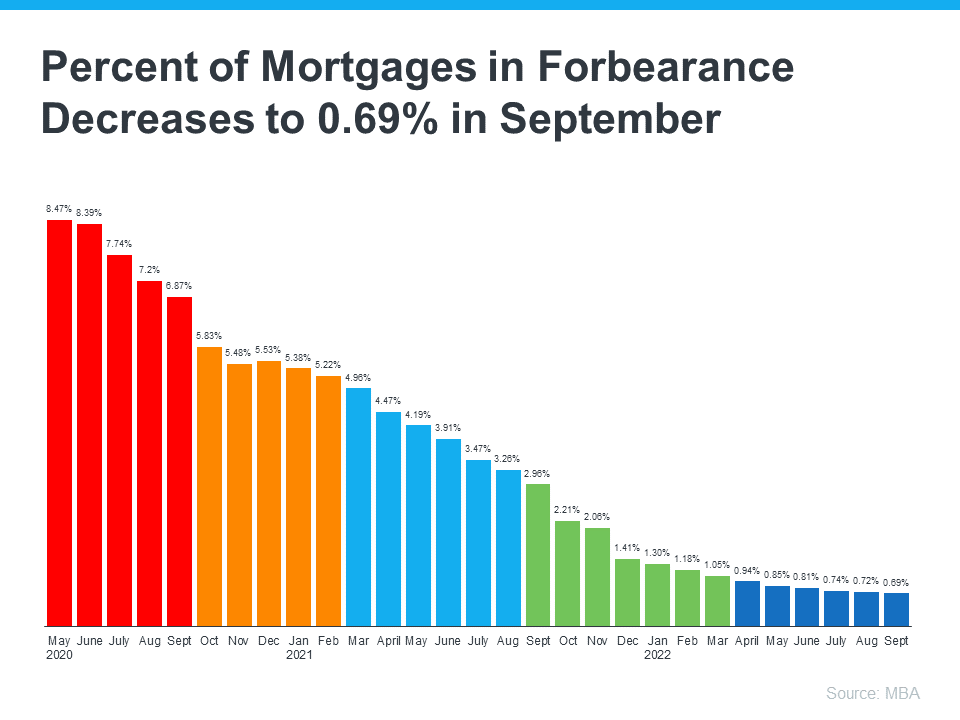

Experts agree there’s no chance of a large-scale foreclosure crisis like we saw back in 2008, and that’s good news for the housing market. As Mark Fleming, Chief Economist at First American, says:

“. . . don’t expect a housing bust like the mid-2000s, as lending standards in this housing cycle have been much tighter and homeowners have historically high levels of home equity, so there likely won’t be a surge in foreclosures.”

Data from the Mortgage Bankers Association (MBA) helps tell this story. It shows the overall percentage of homeowners at risk is decreasing significantly with time (see graph below):

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

“Typically, default is triggered when a borrower misses a specific number of monthly payments . . . Foreclosure is the legal process by which a lender attempts to recover the amount owed on a defaulted loan by taking ownership of and selling the mortgaged property.”

The good news is there are alternatives available to help you avoid going through the foreclosure process, including:

- Reinstatement

- Loan modification

- Deed-in-lieu of foreclosure

- Short sale

But before you go down any of those paths, it’s worth seeing if you have enough equity in your home to sell it and protect your investment.

You May Be Able To Use Your Equity To Sell Your House

Equity is the difference between what you owe on the home and its market value based on factors like price appreciation.

In today’s real estate market, many homeowners have far more equity in their homes than they realize due to the home price appreciation we’ve seen over the past few years. According to CoreLogic:

“The total average equity per borrower has now reached almost $300,000, the highest in the data series.”

So, what does that mean for you? If you’ve lived in your house for at least a few years or more, chances are your home’s value, and your equity, has risen dramatically. In addition, the mortgage payments you’ve made during that time chipped away at the balance of your loan. If your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage.

Rick Sharga, Executive VP of Market Intelligence at ATTOM Data, explains how equity can help:

“Very few of the properties entering the foreclosure process have reverted to the lender at the end of the foreclosure. . . We believe that this may be an indication that borrowers are leveraging their equity and selling their homes rather than risking the loss of their equity in a foreclosure auction.”

Lean on Experts To Explore Your Options

To find out how much equity you have, work with a local real estate professional. They can give you an estimate of what your house could sell for based on recent sales of similar homes in your area. You may be able to sell your house to avoid foreclosure.

If you find out you have to pursue other options, your agent can help with that too. They’ll be able to connect you with other professionals in the industry, like housing counselors, who can look into your unique situation and offer advice on next steps if selling isn’t your best alternative.

Bottom Line

If you’re a homeowner facing hardship, let’s connect so you have an expert on your side to explore your options and see if you can sell your house to avoid foreclosure.

Key Factors Affecting Home Affordability Today

Every time there’s a news segment about the housing market, we hear about the affordability challenges buyers are facing today. Those headlines are focused on how much mortgage rates have climbed this year. And while it’s true rates have risen dramatically, it’s important to remember they aren’t the only factor in the affordability equation.

Here are three measures used to establish home affordability: home prices, mortgage rates, and wages. Let’s look closely at each one.

1. Mortgage Rates

This is the factor most people are focused on when they talk about homebuying conditions today. So far, current rates are almost four full percentage points higher than they were at the beginning of the year. As Len Kiefer, Deputy Chief Economist at Freddie Mac, explains:

“U.S. 30-year fixed mortgage rates have increased 3.83 percentage points since the end of last year. That’s the biggest year-to-date increase in rates in over 50 years.”

That increase in mortgage rates is impacting how much it costs to finance a home purchase, creating a challenge for many buyers that’s pricing some out of the market. While the current global uncertainty makes it difficult to project where mortgage rates will go in the future, experts do say that rates will likely remain high as long as inflation does.

2. Home Prices

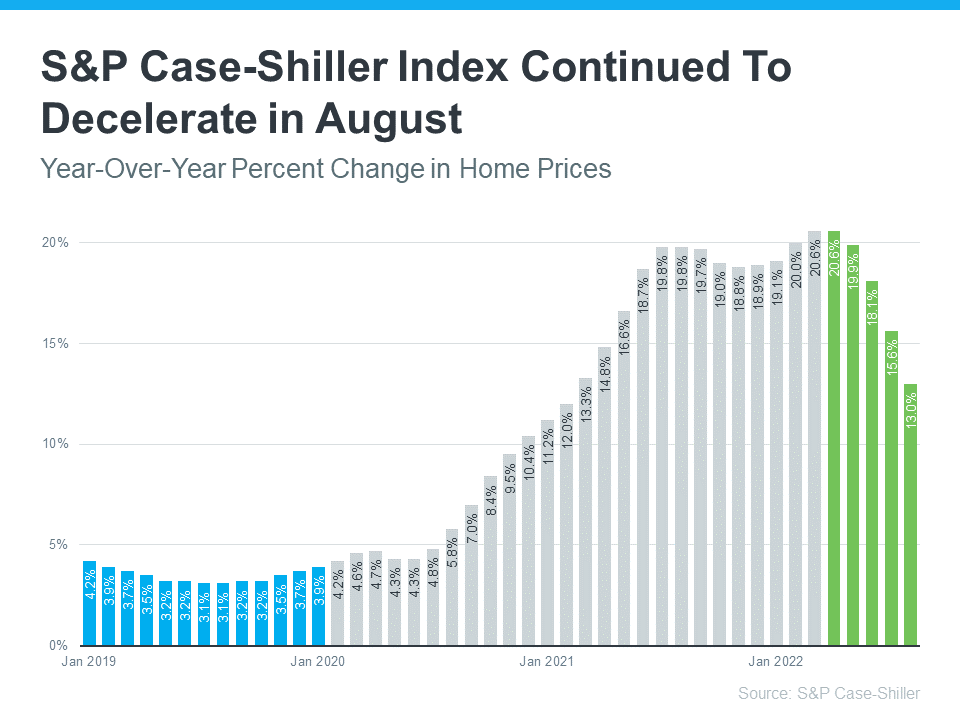

The second factor at play is home prices. Home prices have made headlines over the past few years because they skyrocketed during the pandemic. Now, the most recent Home Price Index from S&P Case-Shiller shows home values continued to decelerate for a fifth consecutive month (shown in green in the graph below):

This deceleration is happening because higher mortgage rates are moderating demand, and as a result, easing the buyer competition and bidding wars that previously drove prices up.

What’s worth noting though, is how much higher home prices still are than they were before the pandemic (shown in blue in the graph above). Even now, we have a long way to go to get to more normal levels of home price appreciation, which is historically closer to 4%. When both mortgage rates and home prices are high, affordability and your purchasing power become a greater challenge.

But while prices are still elevated in many markets, some areas are seeing slight declines. It all depends on your local market. For insight into what’s happening in your area, reach out to a trusted real estate professional.

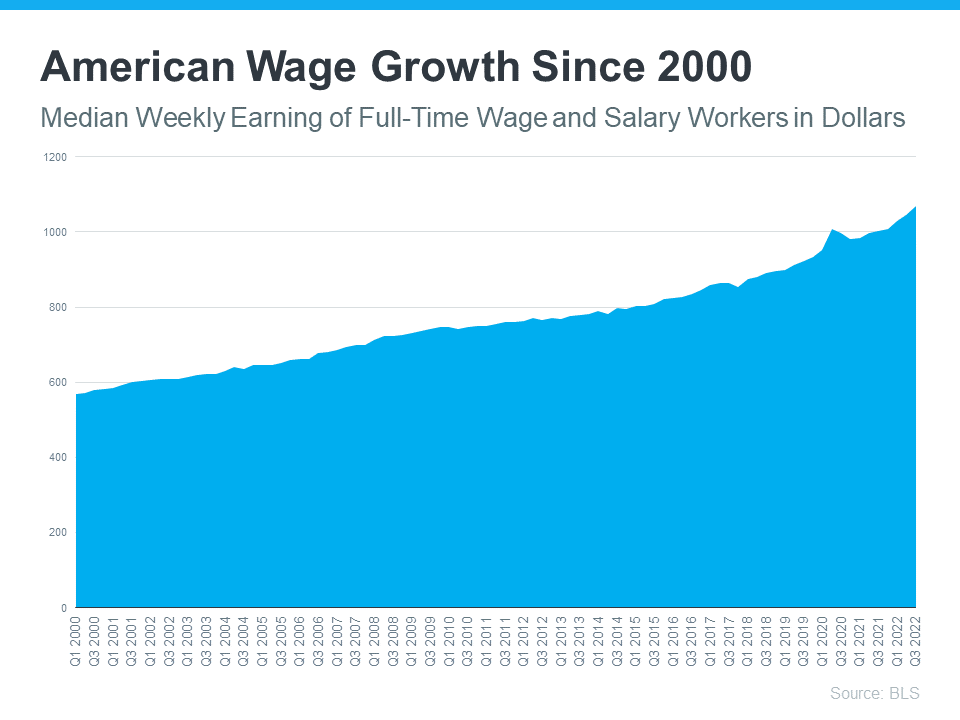

3. Wages

The one big, positive component in the affordability equation is the increase in American wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time. This year is no exception.

As the Bureau of Labor Statistics (BLS) reports:

“Median weekly earnings of the nation’s 120.2 million full-time wage and salary workers were $1,070 in the third quarter of 2022 (not seasonally adjusted), the U.S. Bureau of Labor Statistics reported…This was 6.9 percent higher than a year earlier…”

So, when you think about affordability, remember the full picture includes more than just mortgage rates. Home prices and wages need to be factored in as well. Because wages have been rising, they’re a big reason why serious buyers are still purchasing homes this year.

If you have questions or want to learn more, reach out to a trusted advisor who can explain how all of these variables work together and what’s happening in your area. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

“Buying or selling a home involves a series of requirements and variables, and it’s important to have someone in your corner from start to finish to make the process as smooth as possible… and objectivity to deliver trusted expertise to consumers in every U.S. ZIP code.”

Bottom Line

To learn more, let’s connect today and make sure you have a trusted lender so you’re able to make an informed decision if you’re planning to buy or sell a home right now.